As I write this column, the industry has filed multiple lawsuits and is facing one of the most important legal battles in the past decade. It’s a battle against formidable forces — the Department of Labor and President Barack Obama. At stake are billions of dollars of premium and a lot of companies’ futures. Regardless of the outcome, you can rest assured that big changes are on the horizon. Uncertainty will continue to surround our business well into the foreseeable future.

Tag: marketing strategy

This past December, I attended Dan Kennedy’s two-and-a-half-day Media Mastermind meeting in Cleveland, Ohio. In the room were 18 people from different industries, all with one goal in mind: to increase their presence in their market using media and marketing.

Over the course of my 24-year-long career in the insurance and financial industry, I’ve certainly seen a lot. But one thing that continues to irk me is how poorly we continue to market as an industry. When I started InsuranceNewsNet, I aimed to change that, but I’m sad to report that today I still see financial companies trying 20-year-old marketing tactics that didn’t work then and won’t work today.

It’s understandable. Comfort zones are… comfortable. Plus there’s that old expression “If it ain’t broke, don’t fix it,” but I have to tell you, folks, they’re broke.

How would you like to add some rocket fuel to your sales in 2016? Imagine if it were possible to do this without working harder and with less stress. If you are like most, you love the idea, but you’re not sure exactly how to pull it off. The answer is simpler than one would expect, and it doesn’t require reengineering your entire company or hiring any additional staff.

Regardless of how 2015 went for your company, there is always room for improvement, and there have been many opportunities that you knowingly — or more likely unknowingly — missed out on.

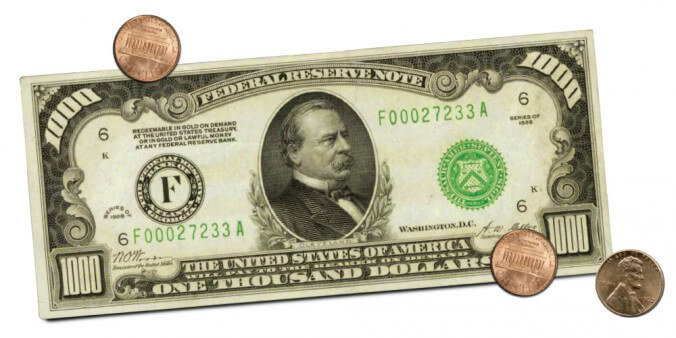

If someone offered you a dollar in exchange for 50 cents, how much would you give? If you are like most, you would probably give everything that you had (I know I would). Ben Feldman sold life insurance for pennies on the dollar. In fact, he used to carry a $1,000 bill with him, which he would tell prospects he would sell to them for 3 pennies.

It’s a great strategy for selling and is an excellent analogy for marketing. Too many companies look at marketing and advertising as an expense – not as an investment. When budget time comes around, the first thing people look to cut is marketing, especially if sales are flat or declining.

If you want to attract more business and grow your existing relationships, I suggest you pay close attention to this month’s issue. While we are going to cover a lot of great strategies, the one you should be paying closest attention to, “Content Marketing” (CM), is perhaps the biggest needle mover for your business and market position.

If you want to attract more business and grow your existing relationships, I suggest you pay close attention to this month’s issue. While we are going to cover a lot of great strategies, the one you should be paying closest attention to, “Content Marketing” (CM), is perhaps the biggest needle mover for your business and market position.

If you are familiar with Content Marketing and think you can skip this part, don’t (because it’s too important). If you’re not familiar with CM or think it’s a fad, it’s NOT. The overall concept has been around for decades (if not centuries) and has been proven to be effective. In the past few years we have tracked thousands of campaigns, and the most successful ones all had an element of content marketing.

They say that half of a loaf of bread is better than no bread at all, and the same is true for your marketing. All too often companies struggle with a sea of options to create the perfect marketing message and to find the perfect platform.

They say that half of a loaf of bread is better than no bread at all, and the same is true for your marketing. All too often companies struggle with a sea of options to create the perfect marketing message and to find the perfect platform.

When Apple introduced the Macintosh in 1984, they knew their product wasn’t perfect. It didn’t have the best hardware, the greatest software, and it was really expensive at $2,495 (equivalent to $5,664 in 2015). According to Guy Kawasaki, then “Chief Evanglist” at Apple, their mantra was, “Don’t worry, be crappy, we must get our product to the market now.”

Generating leads and new business is the primary reason why marketing exists. Over the years, marketing has evolved and companies have become increasingly aware of the results. We know that all leads aren’t of equal value to your business, yet there is a fallacy among many marketers in this industry regarding advisor and agent leads and the measurement of cost per lead . All too often I hear companies say that the CPL is the primary measurement and driver of how their companies’ marketing dollars are spent.

If all leads were equal this would be a correct way to measure, but unfortunately that’s not the case. Anyone can create a lead, it’s easy to create an offer and buy a list, but when you are generating responses — how qualified are they? Did you simply get an email address or did you require more information? Such as an address, type of products they sell, amount of production, etc. And most important — are they even qualified to do business with you?

Ever wonder how a company, armed with basically the same products, seems to rise to a different level in what is clearly a crowded and homogenized market? While the core of their business might be the same as everyone else’s and they ebb and flow with the same economic winds and conditions, their business grows while others struggle.

Ever wonder how a company, armed with basically the same products, seems to rise to a different level in what is clearly a crowded and homogenized market? While the core of their business might be the same as everyone else’s and they ebb and flow with the same economic winds and conditions, their business grows while others struggle.

In the past 5 years, we have seen many new marketing organizations and carriers rise from obscurity to the top of the production scoreboards, while their competitors seemed to idly stand by.

Jim Rohn, one of my favorite quotable speakers of all time, said, “It’s not the blowing of the wind that determines your destination. It is the set of the sail. The same wind blows on us all: The wind of disaster, the wind of opportunity, the wind of change, the favorable wind and the unfavorable wind. The difference of where you will arrive in 1 year, 2 years or even 5 is not the blowing of the wind; it is the set of the sail.”

A good friend of mine, who is a senior marketing executive at a major carrier, once told me that “every agent you have will leave you. It might be 6 months, 5 years or even 10, but one day they will move on to greener pastures or just die on you.” That’s a scary statement, but unfortunately it’s true.

A good friend of mine, who is a senior marketing executive at a major carrier, once told me that “every agent you have will leave you. It might be 6 months, 5 years or even 10, but one day they will move on to greener pastures or just die on you.” That’s a scary statement, but unfortunately it’s true.

In order for a marketing company or carrier to reach its full sales potential, it must be in front of the market and always looking for new producers. In this industry, it is not uncommon to see 20% turnover of your producers annually. More than half of the annual turnover is typically caused by factors outside of one’s control, such as death, disinterest, lack of business, retiring or changing markets. But the fact remains that in 5 years, you will have to replenish almost all of your producers.